Most practices treat patient payments like something that happens after care — send a bill, hope for the best, maybe call if nothing shows up. Then they wonder why collections drag for months and staff spend half their day chasing down $75 copays from three months ago.

The real issue isn't that patients won't pay. It's that practices wait until after the visit to have financial conversations, when the patient's already gone and staff have moved on to the next fire. By then, you're fighting uphill against confusion, sticker shock, and simple forgetfulness.

A proper patient financial engagement workflow starts way before the appointment and continues through structured touchpoints that make payment feel like a natural part of care — not an ambush. Pre-visit estimates that actually get sent, point-of-service scripts your staff will use, and collection escalation that follows account aging automatically, not whenever someone remembers to pull the AR report.

The pre-visit estimate window nobody gets right

Every practice manager knows they should send estimates before visits. Almost none do it consistently. The breakdown usually happens in one of three places: pulling the estimate takes too long, staff forget to send them, or the timing is completely off.

What actually works: estimates go out 5-7 business days before appointments for scheduled procedures and 48-72 hours for routine visits. Any earlier and patients forget. Any later and they can't arrange payment. The window gives them enough time to call with questions but not so much that the information feels stale.

The estimate itself needs three components most practices miss. First, show the total expected charge, their estimated insurance coverage, and their likely responsibility — but also include a confidence range. Telling someone "your portion will be approximately $340-$420 depending on how your deductible processes" sets better expectations than a precise number that ends up wrong. Second, include payment options right in the estimate. Not "we accept credit cards" — specific paths: pay in full for 5% off, split into two payments, or discuss a monthly plan for balances over $500. Third, add a clear next step. "Please call if you have questions" is useless. Something like "Reply YES to confirm you received this estimate, or call 555-0100 to discuss payment options" actually moves people.

For specialty visits and procedures over $1,000, the estimate should trigger a required financial conversation — not optional, not "if they ask." Schedule these as 10-minute phone appointments 3-4 days before the visit, blocked by the scheduler like any clinical slot. Staff walk through the estimate line by line, confirm insurance details, and document the payment plan. No surprises on visit day.

The estimate process needs ownership and tracking. Assign one person per week to pull and send estimates for the following week's schedule. Track your send rate (estimates sent divided by eligible visits) and your response rate (patients who acknowledge or discuss the estimate). Most practices discover they're sending estimates for maybe 20% of eligible visits. Getting to 80% typically increases point-of-service collections by 40-60%.

Day-of collections that actually happen

Point-of-service collection fails for two reasons: staff hate asking for money, and patients hate being surprised. Fix both with scripts that make payment discussions feel routine and systems that eliminate surprises.

Eliminate appointment gaps and no-shows.

GoCliny streamlines every patient interaction from booking to billing—seamlessly.

- Unified appointment scheduling

- Automated patient reminders

- Staff calendar & task management

No credit card required

Your check-in flow needs a financial touchpoint every single time, not just when someone remembers. After insurance verification, before clinical check-in, the front desk pulls up the patient's financial summary — estimate, previous balance, today's expected responsibility. The script is simple: "I'm showing your estimated portion for today's visit is $165 after insurance. How would you like to take care of that?"

Make the payment question part of the standard check-in script so staff don't have to decide when to bring it up.

Notice what that script doesn't do. It doesn't apologize. It doesn't make payment optional. It doesn't wait until after the visit when the patient's rushing to leave. It assumes payment will happen and only asks about method.

For patients who push back, you need escalation paths, not arguments. Level one: "I understand. Let me pull up your payment options — we can split this into two payments, or I can connect you with our financial counselor to discuss a monthly plan." Level two: "Our policy requires payment or payment arrangements before non-emergency services. Would you prefer to handle this today or reschedule once you've arranged payment?" Level three involves the practice manager or designated financial counselor who has authority to approve exceptions.

Checkout needs its own financial checkpoint too. Even if payment was collected at check-in, staff confirm the amount and method: "We collected your $165 copay at check-in. Your insurance will receive the remaining charges, and you should receive an explanation of benefits in 2-3 weeks." This prevents the confused calls three weeks later asking what some random charge on their card was for.

For procedures and higher-dollar visits, implement a financial consent process — not just signing a form. The patient reviews a written summary of charges and their expected responsibility, initials each section, and signs acknowledgment. One practice started requiring this for all procedures over $500 and saw their 30-day collection rate jump from 45% to 78%.

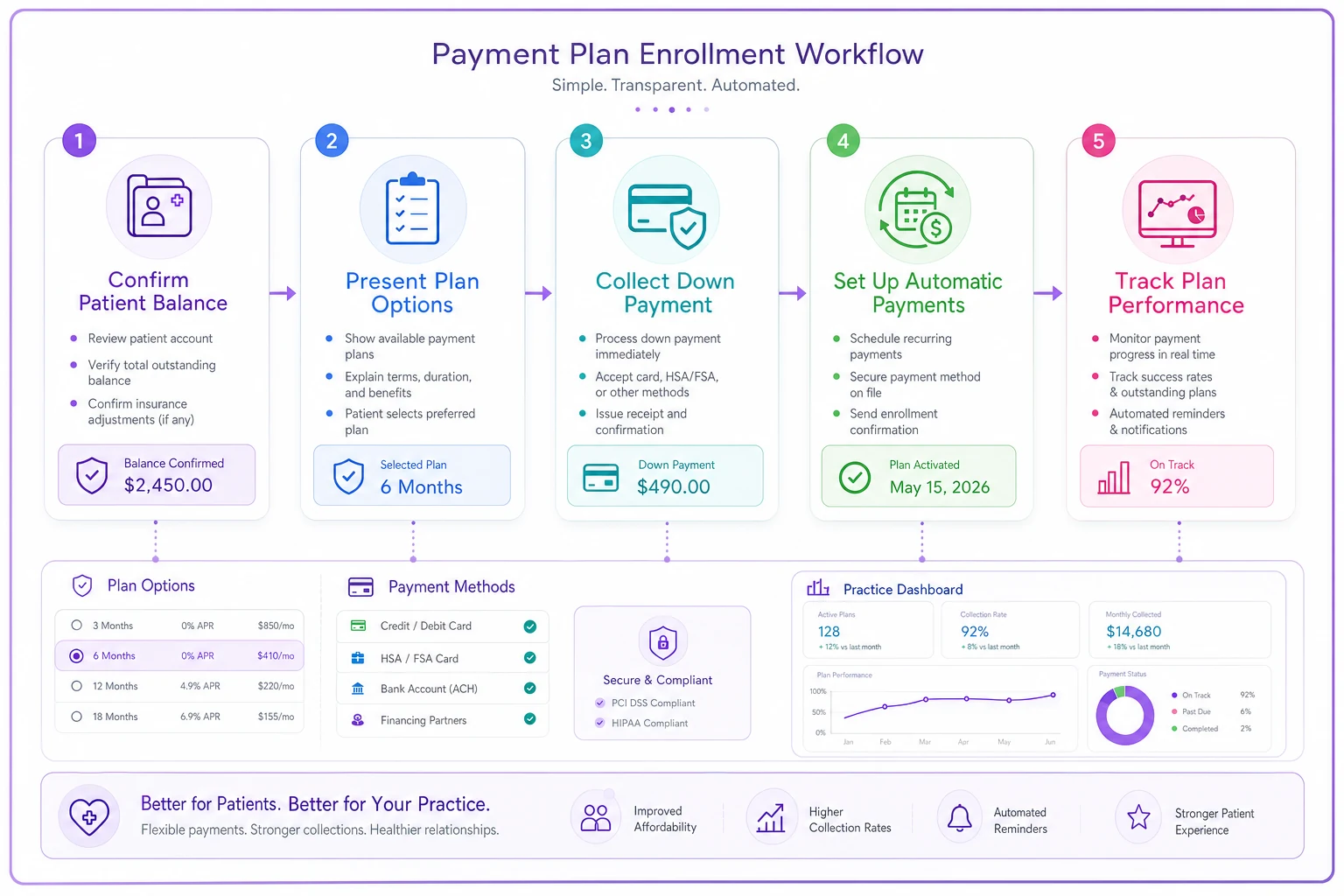

Payment plan workflows that scale

Payment plans multiply your administrative burden unless you build them right from the start. Most practices create custom plans for each patient, track them in spreadsheets, and manually process payments. This works for maybe five plans. By twenty, someone's missing payments and nobody knows who owes what.

| Balance Range | Standard Plan |

|---|---|

| Under $500 | two equal payments, first due immediately, second in 30 days. |

| $500-1,500 | three to six monthly payments with 20% down required. |

| Over $1,500 | up to 12 months with 25% down, requires financial counselor approval. |

Start with standard plan templates based on balance ranges. Under $500: two equal payments, first due immediately, second in 30 days. $500-1,500: three to six monthly payments with 20% down required. Over $1,500: up to 12 months with 25% down, requires financial counselor approval. Standard options speed up decisions and create consistency.

The enrollment conversation follows a specific flow. First, confirm the total balance and explain how it was calculated. Second, present the standard plan options for that balance range. Third, calculate the monthly payment and confirm the patient can commit to it. Fourth, get the down payment immediately — not tomorrow, not next week, right now while you have them on the phone. Fifth, set up automatic payments for the remaining balance.

Below is a visual of the payment plan workflow.

Document every plan in a standard format: total balance, payment schedule, payment method, what happens if they miss a payment, who approved any variations from standard terms. Store this in your practice management system, not in random spreadsheets. The patient gets a copy immediately via email or patient portal.

Automatic payment processing is non-negotiable for plans over three months. Recurring charges on the same day each month. Reminder emails three days before each charge. If a payment fails, the patient gets an immediate notification and the account gets flagged for follow-up within 24 hours.

Track plan performance closely. What percentage of plans complete successfully? What's your average default point? One practice found their morning front desk person's payment plans had a 90% completion rate while the afternoon person's sat at 60%. The difference: the morning person always got the down payment immediately, while the afternoon person let patients "come back tomorrow" to make the first payment. Most never did.

Collection escalation that follows rules, not feelings

Collections fail when they depend on someone remembering to check aging reports and deciding who to call. Escalation rules should trigger automatically based on account age and balance — not when someone feels like making uncomfortable calls.

Your escalation ladder needs clear stages with specific actions:

-

Days 0-30 Email and text reminders every 7 days, automated.

-

Days 31-45 Personal phone call attempt, voicemail if no answer, email summary of the attempt.

-

Days 46-60 Formal letter via mail and email, payment plan offer included, hold on scheduling non-urgent appointments.

-

Days 61-75 Final notice letter, warning of potential collection agency placement.

-

Days 76-90 Supervisor review for write-off or collection agency placement.

Each stage needs clear ownership. Accounts 0-30: handled by automated systems with front desk oversight. Accounts 31-60: assigned to specific billing staff on rotation. Accounts 61-90: escalated to billing supervisor or practice manager. Over 90 days: reviewed by practice administrator for final disposition.

Script templates remove the guesswork from collection calls. The 31-day call: "I'm calling about your balance of $287 from your September visit. I show we sent statements on September 20th and 27th. Can we arrange payment today?" The 45-day call: "Your account is now past due. To avoid further collection activity, we need to establish a payment arrangement today. I can take payment now or set up a short payment plan." The 60-day call: "Your account will be reviewed for collection agency placement in 15 days unless we receive payment or establish a payment plan. This is something we want to avoid — what arrangement can we make today?"

Build stopping rules too. Stop calling if three attempts over two weeks get no response — move to written notices only. Stop everything if the patient disputes the charge — route to billing supervisor for resolution. Stop collection efforts if the balance drops below your cost threshold (usually $25-50) — write these off in quarterly batches.

The key metric isn't how many calls you make but how many accounts move to resolution. Most practices find around 60% of past-due accounts resolve after the first personal contact if it happens within 35 days. Wait until day 60 and that rate drops to roughly 30%.

KPI triggers that force action

Your patient financial engagement workflow needs measurement points that trigger specific actions — not just numbers sitting on a report. Build these into your monthly operational dashboard with clear thresholds and required responses.

Point-of-service collection rate below 65%: Triggers immediate retraining on collection scripts and check-in workflows. Below 50%: requires daily huddles on collection performance until the rate improves. Not punitive — it's recognizing that something in your process is broken.

Estimate send rate below 75%: Triggers an audit of the estimate preparation process. Who's responsible? What's blocking them? Below 60%: implement daily estimate preparation instead of weekly batches, with manager spot-checks until the rate recovers.

Payment plan default rate above 20%: Triggers review of plan terms and down payment requirements. Are plans getting approved for patients who clearly can't commit? Are the monthly amounts too high? Above 30%: require financial counselor approval for all new plans.

Days in AR above 45: Triggers immediate review of collection processes. Which stages are creating bottlenecks? Are staff actually making their assigned calls? Above 60: implement daily aging review meetings until AR drops back below threshold.

These triggers need teeth. Not "we should look into this" but "this specific person must take this specific action within 24 hours." The billing supervisor can't just note that collection rates are low — they must schedule retraining within three business days. The practice manager can't just express concern about AR days — they must personally review every 60+ day account within one week.

ROI examples that justify the effort

A 25-provider primary care practice implemented structured pre-visit estimates and saw their point-of-service collections increase from roughly $47,000 to $76,000 monthly within four months. The main change was straightforward: sending estimates to everyone with a balance over $100, not just for procedures. Their billing staff spent less time on collection calls because patients arrived expecting to pay.

A surgical practice with chronic collection problems built a strict payment plan workflow with required down payments and automatic monthly charges. Their plan completion rate went from 45% to 82%. More importantly, their 90-day AR dropped by $180,000 over six months. The key wasn't approving fewer plans — it was enforcing the down payment requirement and setting up automatic payments during the initial conversation.

An urgent care network standardized their collection escalation across five locations. Previously, each location handled collections differently, with success rates on 30-day accounts varying from 30% to 65%. After implementing consistent scripts, ownership assignments, and escalation triggers, all locations landed in the 55-60% range. Their cost per dollar collected dropped from $0.31 to $0.19.

Sample scripts that staff will actually use

Check-in collection script: "Good morning! I show your copay for today is $40, and you have a previous balance of $127 from your August visit. Your total due today is $167. Will that be card or check?"

If the patient objects: "I understand. For the copay, that's required at time of service per your insurance. For the previous balance, I can offer you two options: pay half today and half in 30 days, or speak with our financial counselor about a monthly payment plan. Which would work better?"

Pre-procedure financial consent call: "This is Sarah from Dr. Johnson's office calling about your upcoming procedure on Thursday. I'm calling to review your cost estimate and arrange payment. Based on your insurance verification, your estimated portion will be $1,850. This includes your remaining deductible of $800 and 20% coinsurance. Do these numbers match what you were expecting?"

If they weren't expecting it: "I understand this might be higher than anticipated. Let me explain how we calculated this amount... [explanation]. For amounts over $1,000, we require a 25% deposit before the procedure and can arrange monthly payments for the balance. With 25% down, your monthly payment would be about $470 for three months or $240 for six months. Which timeline would work better for your budget?"

Collection escalation call (45 days): "This is Mike from City Medical billing. I'm calling about your balance of $423 from your September visits. Our records show we've sent two statements, and I wanted to reach out personally to help resolve this. Can we arrange payment today, or would you prefer to set up a payment plan?"

Decision trees that eliminate confusion

When a patient says they can't pay the full amount at check-in, your staff needs a clear path, not a panic moment. Here's the decision flow:

Is it a copay or deductible? If yes: Payment is required per insurance contract. Offer to reschedule if they cannot pay. If no: Continue to next question.

Is the balance over $500? If yes: Route to financial counselor for payment plan discussion. If no: Offer standard two-payment split.

Has this patient defaulted on a previous plan? If yes: Require 50% down for any new arrangement. If no: Standard 20% down minimum.

Is this an urgent or emergent visit? If yes: Provide care and arrange payment plan after visit. If no: Require payment arrangement before service.

Your revenue cycle framework needs these decision points built in at every stage, not just at the point of service.

The operational software angle

Manual patient financial engagement workflows break down at scale. When you're tracking 50 payment plans in spreadsheets, sending individual estimate emails, and hoping someone remembers to call overdue accounts, things fall through the cracks.

AI-powered operational platforms handle the repetitive parts while your staff focus on actual conversations — automated estimate generation based on CPT codes and insurance verification, triggered payment reminders that adjust tone based on account age, payment plan tracking that flags at-risk accounts before they default, and collection workflow assignment that ensures every account gets worked at the right time.

The real value isn't replacing human judgment. It's eliminating the manual tracking that makes consistent execution impossible. Your billing supervisor shouldn't spend mornings figuring out who needs to be called — the system should present a prioritized work queue based on your escalation rules. Your front desk shouldn't have to remember to ask for payment — the check-in screen should prompt them with the exact amount due and acceptable payment options.

These platforms also learn from your successful collections over time. If Thursday afternoon payment reminder emails get meaningfully better response than Monday morning ones, the system adjusts. If patients under 35 respond better to text than email, it adapts. If certain insurance plans consistently underpay estimates, it factors that into future calculations.

Why this beats hoping for the best

Building a patient financial engagement workflow isn't about being aggressive with collections. It's about setting clear expectations, removing surprises, and making payment as frictionless as possible. Patients actually prefer knowing what they'll owe upfront, even when the number is uncomfortable.

The practices that excel at patient collections don't have better patients or more aggressive staff. They have better systems. Estimates go out automatically. Payment discussions follow scripts. Escalation happens on schedule. KPIs trigger specific actions. They've turned an uncomfortable, inconsistent process into a predictable operational workflow.

Your pre-submission QC workflow ensures clean claims — but that's only half the revenue cycle. The other half is actually collecting what patients owe. Without a structured financial engagement workflow, you're leaving money on the table and creating unnecessary friction with patients who just want clarity about their financial responsibility.

Start with one piece — pre-visit estimates for procedures over $500. Get that running consistently for a month. Then add point-of-service scripts. Then payment plans. Then automated escalation. Within six months, you'll have turned patient payments from your biggest operational headache into a reasonably predictable revenue stream.

The goal isn't perfection. Some patients still won't pay. Some plans will default. Some conversations will be uncomfortable. But with the right workflow in place, these become exceptions to manage, not the daily chaos your billing staff wade through while your AR quietly ages into uncollectible territory.

Ready to transform your practice workflow?

Join 2,000+ healthcare providers using GoCliny to increase efficiency, improve patient satisfaction, and grow revenue.